Commentary

The latest released U.S. nonfarm payrolls continue on the upside to the surprise of the market, with a month-on-month (MoM) increase of 253,000 jobs beating expectations of 180,000 and the previous month’s 165,000. Despite the trend has been declining from 400,000 at the beginning of the year to over 200,000, which is not low by any standard. During the 2010s, the normal boom years, the stable average was 200,000, but fluctuated between 100,000 and 300,000. It seems very hard to imagine how a recession could be on the brink despite the yield curve having a firm prediction to it.

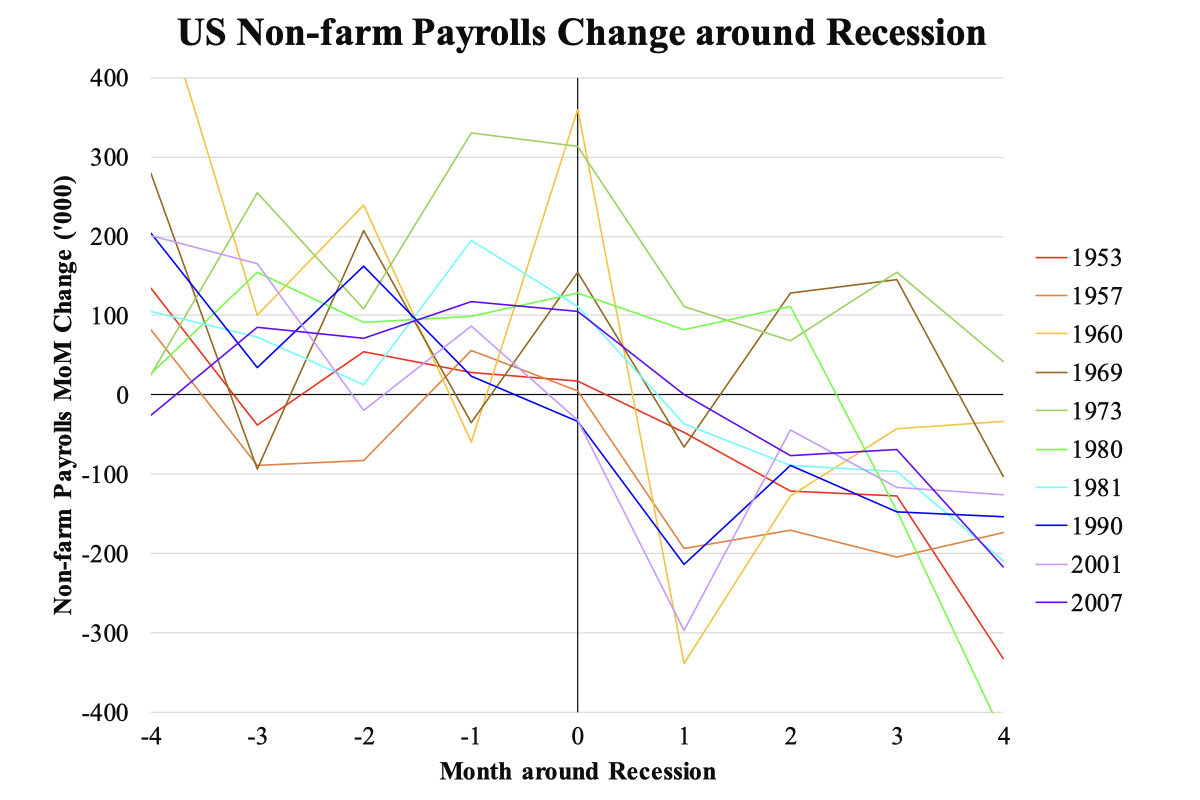

To resolve this anomaly, we could simply review the past experience with historical data. The nonfarm payrolls record goes back to the late 1930s, but there is no harm in focusing on the post-war period. The accompanying chart shows the payrolls trend around the beginning of ten recessions, excluding the COVID-19 one in 2020 (where that recession was highly artificial due to lockdowns). Along the time axis, “0” refers to the beginning month of a recession defined by the National Bureau of Economic Research (NBER), and a neighbouring four months before and after are shown.

Illustration of US Non-farm Payrolls Changes around Recession, May 8, 2023. (Courtesy of Law Ka-chung)

Illustration of US Non-farm Payrolls Changes around Recession, May 8, 2023. (Courtesy of Law Ka-chung)

A glance at time 0, when a recession just started, there was still decent job growth at over 100,000 in 6 out of 10 cases. In only two cases (1990 and 2001) where recessions were short and mild, had jobs cut when the recession just began. Only one month after the recession started (month 1) would most cases (8 out of 10) have job cuts, yet there were a few cases of job growth in the second and third months of the recession. Payroll is not a lagger, calculation (moving correlation) shows it is coincident or very slightly leading. But it is theoretically not a predictor of recession.

Recession is defined by real activities (output) going from peak to trough. By definition, the overall economy should be at its peak at the onset of the recession. It follows that any sign of contraction should happen in the first month (month 1) at the earliest. Since payroll is one of the six indicators used by NBER to define recession, payroll per se cannot be a leading indicator.

Because laying off and cutting spending does not take much time to work through (unlike stopping a production line), a contraction in payroll and consumption can happen instantly when a recession begins. Economic theories prescribe demand (whether labor or goods) can be altered without lag (unlike supply which takes time to stop), demand data do not have predictive power.

In order to anticipate the future, one has to resort to supply-side data like investment or production, which span across time. Nevertheless, most data on the table have shown clearly that investment-related activities and production (such as manufacturing PMI) have been weakening for a long time. These are already strong signals beyond the yield curve in predicting a recession.

Now is not a yes-no question, but when. History shows recession would materialize after one to two-quarters of the first-round crisis. The chance to kick start by fall 2023 is still very high.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.